Reduced minimum pension – Planning Opportunity

As part of the Federal Government’s economic response to COVID-19, the minimum percentage withdrawals from superannuation pension accounts were reduced by 50% as from 24/3/2020 and this is to apply for the 2019-20 and 2020-21 financial years.

This will enable self funded retirees to potentially reduce their pension withdrawals for a period in order to preserve asset values and avoid selling growth assets in a depressed market.

However, there may be cases where the member still requires a higher pension amount and in those cases, consideration should be given to taking the extra amount as a commutation/lump sum. This has the advantage of reducing the member’s Transfer Balance Cap, thus providing space for potential further transfers into pension mode in the future. The advantage of pension mode accounts is that all income and capital gains derived in those accounts will be tax free.

Example:

Mary is aged 68 and currently has a sole member SMSF with a retirement phase pension account balance of $1,550,000. Her Transfer Balance Cap is $1,600,000. Her minimum pension was previously 6% or $93,000 but under the changes, that minimum is reduced to 3% or $46,500. For various reasons, Mary does not wish to reduce her pension withdrawals and therefore will withdraw $93,000 in the current financial year – $46,500 was withdrawn in December and she plans to withdraw a further $46,500 in June 2020. If Mary treats the full $93,000 as a pension, her Transfer Balance Cap will not change and she will have no further ability to transfer additional amounts into pension mode. On the other hand, if Mary decides to take the June payment as a commutation from her pension account and then as a lump sum from the accumulation account, her Transfer Balance Cap will reduce by $46,500 and that amount could be re-contributed in the future and then transferred to pension mode, thus increasing the actual superannuation amount in pension phase.

Note that commutations need to be properly documented and reported to the regulator in the appropriate way.

The information provided in this article is general in nature and does not take into account your personal circumstances, needs, objectives or financial situation. This information does not constitute financial or taxation advice. Before acting on any information in this article, you should consider its appropriateness in relation to your personal situation and seek advice from an appropriately qualified and licensed professional.

BOB LOCKE – CHARTERED ACCOUNTANT & SMSF SPECIALIST

Mr Locke has been an accountant and taxation expert for 35 years. His company, Practical Systems Super, provides an all-in-one SMSF solution with a full administrative service, SMSF management software, and independent, licensed advice, tailoring their package to meet the individual needs of trustees and SMSF professionals.

To find out more about Practical Systems Super, visit www.pssuper.com.au, or call 1800 951 855.

TIME TO TRANSFER SHARES TO YOUR SMSF?

One of the few exceptions where personal assets can be transferred “in-specie” to a Self-Managed Superannuation Fund, is listed shares. These, of course, have to be transferred at market value and therefore a potential barrier to these transfers is often the capital gain that may be generated by the individual as a result of the transfer.

With the significant downturn in markets as a result of the COVID-19 crisis, it may be a good time to consider transfers as there may be minimal capital gains tax effect on the transfer. It may also be possible to treat some or all of the in-specie transfer as a concessional contribution and therefore improve the overall tax effectiveness. Obviously, where transfers are to be treated as contributions, it will be necessary to ensure that you take account of relevant contribution caps applying to the member.

The information provided in this article is general in nature and does not take into account your personal circumstances, needs, objectives or financial situation. This information does not constitute financial or taxation advice. Before acting on any information in this article, you should consider its appropriateness in relation to your personal situation and seek advice from an appropriately qualified and licensed professional.

BOB LOCKE – CHARTERED ACCOUNTANT & SMSF SPECIALIST

Mr Locke has been an accountant and taxation expert for 35 years. His company, Practical Systems Super, provides an all-in-one SMSF solution with a full administrative service, SMSF management software, and independent, licensed advice, tailoring their package to meet the individual needs of trustees and SMSF professionals.

To find out more about Practical Systems Super, visit www.pssuper.com.au, or call 1800 951 855.

How is your SMSF performing?

With over 600,000 funds and an average balance of around $1.2 Million, Self-Managed Superannuation Funds (SMSFs) make up for a significant portion of total superannuation assets in Australia.

One of the main reasons that SMSFs are a popular choice for Australians in their retirement planning, is that individuals feel they have control over their retirement savings. However, with this decision making power comes responsibility. Some SMSF trustees manage all of the fund investments while others use an investment adviser to provide this service. Many also use a combination of both approaches – for example, they may attend to direct property themselves and use an investment adviser to look after the equities portion of the portfolio.

While some Trustees would have a very good knowledge of the investment returns and costs of their fund, many are left to interpret their statutory annual reports for this. These reports are often directed at compliance experts and it can be difficult for Trustees to fully understand how their investments are tracking relative to other indicators such as industry funds or investment benchmarks.

Calculating your SMSF performance

The idea of analysing the statutory report and extracting the performance information may seem daunting but can be quite simple. It’s just a matter of applying a formula to the relevant set of numbers.

Here’s how a Trustee could calculate the investment performance by using the Fund’s annual Operating Statement and Balance Sheet reports.

From the Operating Statement:

A. Calculate Gross investment income – be sure to leave out member contributions and any amounts rolled into the fund

B. Calculate investment related expenses – leave out member withdrawals, life insurance premiums and general administration expenses such as audit & accountancy fees

C. Net investment return (before tax) = A – B

D. Calculate the income tax expense (or refund) that relates to the net investment income – exclude the tax (15%) applicable to any concessional contributions

E. Investment return after tax = C – D

From the Balance Sheet:

F. Calculate average assets for the year – this will usually be the opening and closing net assets divided by 2 but a more sophisticated approach would be to use say a monthly weighted average of net assets to recognize significantly contributions/withdrawals during the year

The after-tax return % = E divided by F x 100

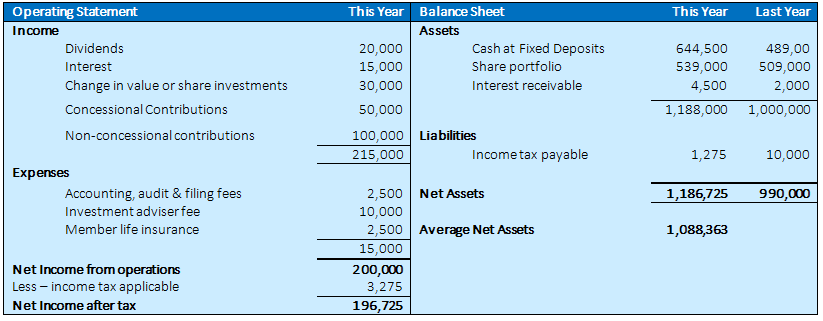

The practical application of this relatively simple process can be illustrated in the following example

Applying the formula to the above example, the components are:

A (investment income) = $20,000 + $15,000 +$30,000 = $65,000

B (investment expenses) = $10,000

C (net investment return) = $65,000 – $10,000 = $55,000

D (tax related to investment return) = $4,225 credit ($7,500 relates to concessional contributions less $4,225 = $3,275)

E (investment return after tax) = $55,000 + $4,225 (tax credit) = $59,225

F (average assets) = ($1,186,725 + $990,000) / 2 = $1,088,363

E (investment return after tax) = ($59,225 / $1,088,363) x 100 = 5.44%

Another important ratio that trustees may be interested in, is administration expenses as a percentage of average assets. Using the above sample data this would be calculated as:

- Administration expenses = $2,500 divided by average assets $1,088,363 x 100 = 23 %

Having calculated these ratios, the obvious question is; “how do these compare to other superannuation funds or alternatives?”. There are several “benchmarks” that a fund could choose to look at for comparison purposes. The Australian Taxation Office does provide some data, but this is limited and tends to be quite dated by the time it is released.

Some other possible benchmarks might include:

- All Ordinaries Accumulation Index: this provides the return from a theoretical basket of investments representing the All Ordinaries Index on the Australian Share Market including growth in value and dividends (grossed up by franking credits). It is, therefore, a useful benchmark for portfolios of listed Australian Shares. As an example, this index rose by 11.03% for the year ended 30th June 2019.

- Indices relating to specific investment sectors such as property, fixed interest, etc.

- Returns from the large Industry Funds: these are published and available for various member-selected investment mix options. As an example, the return for the “balanced fund” option of Australian Super for the year ended 30th June 2019 was 8.67%

- Returns compiled by investment research firms such as Chant West or MSCI

- Returns achieved by various index funds and Exchange Traded Funds

When comparing SMSF returns and costs to benchmarks and other alternatives it is important to take account of unique and particular issues that may affect the data in the different sectors. Some examples of these issues include:

- SMSFs would rarely revalue direct property investments every year

- An SMSF fully in pension mode with a significant share portfolio paying franked dividends would be expected to have a higher after-tax return than if the same fund was in accumulated phase.

- Some administration cost of industry or retail funds may be “hidden” in net investment returns.

To get a quick comparison of the administration cost structure for your SMSF, complete the form below and a Practical Systems Super representative will be in touch.

The information provided in this article is general in nature and does not take into account your personal circumstances, needs, objectives or financial situation. This information does not constitute financial or taxation advice. Before acting on any information in this article, you should consider its appropriateness in relation to your personal situation and seek advice from an appropriately qualified and licensed professional.

BOB LOCKE – CHARTERED ACCOUNTANT & SMSF SPECIALIST

Mr Locke has been an accountant and taxation expert for 35 years. His company, Practical Systems Super, provides an all-in-one SMSF solution with a full administrative service, SMSF management software, and independent, licensed advice, tailoring their package to meet the individual needs of trustees and SMSF professionals.

To find out more about Practical Systems Super, visit www.pssuper.com.au, or call 1800 951 855.

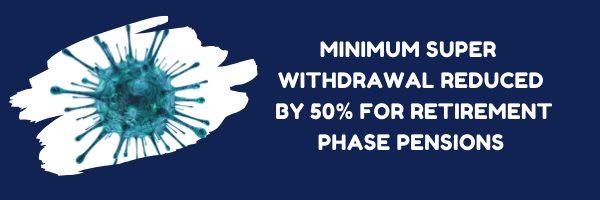

Minimum super withdrawal reduced by 50% for retirement phase pensions

IMPORTANT: Minimum super withdrawal reduced by 50% for retirement phase pensions

In response to the COVID-19 pandemic, the Federal Government recently announced that the minimum superannuation drawdown rate would be halved for the 2019/20 and 2020/21 financial years. This measure is designed to benefit retirees by reducing the potential need to sell investment assets into a depressed market to fund their minimum drawdown requirements. See the following table for details:

| Age | Default minimum drawdown rates (%) | Reduced rates by 50 per cent for the 2019-20 and 2020-21 income years (%) |

|---|---|---|

|

Under 65 |

4 |

2 |

|

65-74 |

5 |

2.5 |

|

75-79 |

6 |

3 |

|

80-84 |

7 |

3.5 |

|

85-89 |

9 |

4.5 |

|

90-94 |

11 |

5.5 |

|

95 or more |

14 |

7 |

Please note that if you have already drawn more than your reduced minimum for this financial year, you are unable to return the excess amount.

The information provided in this article is general in nature and does not take into account your personal circumstances, needs, objectives or financial situation. This information does not constitute financial or taxation advice. Before acting on any information in this article, you should consider its appropriateness in relation to your personal situation and seek advice from an appropriately qualified and licensed professional.

Transition to retirement pensions – are they still effective?

As people age, the everyday grind of full-time work can become increasingly tiresome. At the same time, many still enjoy the interest and challenges of the workplace. One way to help with this “work-life balance” at this stage of life is a Transition to Retirement (TTR) strategy.

Transition to retirement strategy explained

If you have reached your preservation age, (between age 55 and age 60 depending on your date of birth) this strategy allows you to reduce working hours and at the same time, commence a special type of pension withdrawal arrangement from your superannuation fund.

This means your take-home pay does not have to be reduced (and potentially increased) but allows more time away from work to experience other aspects of life whilst you’re still active and healthy.

Sometimes these arrangements are coupled with a “re-contribution strategy” where concessional contributions into the fund are maximised using a combination of pension withdrawals and tax savings to cover any shortfall in disposable income.

The table below outlines the preservation age applying to an individual:

| Date of Birth | Preservation age |

|---|---|

|

Before 1/7/1960 |

55 |

|

1/7/1960 to 30/6/1961 |

56 |

|

1/7/1961 to 30/6/1962 |

57 |

|

1/7/1962 to 30/6/1963 |

58 |

|

1/7/1963 to 30/6/1964 |

59 |

|

After 30/6/1964 |

60 |

Transition to retirement strategy options

- Cut your hours, not income

This strategy focuses on using income from your transition to retirement pension so you can reduce your work hours, enjoy the same level of after-tax income and still maintain your lifestyle. The downside? Your super savings may decrease earlier than expected.

2. Ramp up your super

Choosing this option means you can continue to work full time, make additional super contributions via salary sacrifice and draw an income from your TTR pension to help fund your living expenses.

Remember that your salary sacrifice super contributions are taxed at 15% provided your concessional contributions fall within the applicable super contribution caps, while an additional 15% tax may be applicable for higher-income earners.

While still working full time, the 15% tax rate may potentially be lower than your marginal tax rate had you received this money as salary – this can help to reduce your tax bill and give your retirement savings a boost.

In a nutshell, this transition to retirement strategy allows you to contribute more to super than you draw as an income stream, while keeping your after-tax income the same.

Transition to retirement strategy – is it still relevant?

In the past, one of the significant advantages of a so-called “Transition to Retirement Income Stream” (TRIS) was that the income and capital gains derived in the superannuation fund from assets supporting the TRIS were exempt from tax in the fund.

This concession was removed with the raft of changes that applied to all superannuation funds from 1st July 2017. Note that the receipt of a TRIS by a member over the age of 59 is exempt from income tax and partially exempt for members between preservation age and 59. This aspect has not changed.

A question often asked is, “are transition to retirement strategies still relevant?”. The answer is clearly yes but it also depends on individual circumstances!

The following table summarises Peter’s position regarding annual net salary and annual net increase in his superannuation in three different scenarios.

(a) Current position working full time

(b) Reducing to 3 days a week and not altering existing superannuation arrangements

(c) Reducing to 3 days a week, paying additional concessional super contributions (to max $25,000) and using a transition to retirement strategy to fund these changes and ensure net disposable income remains unchanged..

We can see in (a) that Peter’s current disposable income is $97,903 pa and his annual super balance increase would be expected to be $53,805 – an overall total of $151,708. If he reduces to 3 days per week as in scenario (b), his disposable income reduces by around 35% to $64,553 and his combined total reduces by $37,822 and this would be the effective “cost” (in the first year) of reducing work hours from full time to 3 days per week. On the other hand, scenario (c) illustrates that if Peter implemented a TRIS and withdrew $44,498 from his superannuation to cover the reduction in income and maximize concessional contributions, he could maintain his current disposable income and reduce the overall “cost” from $37,822 to $34,553.

The above example illustrates how a Transition to Retirement Strategy can be used to maintain disposable income where work hours are significantly reduced. Other strategies can revolve around objectives such as paying down debt as a member is approaching retirement, equalizing superannuation balances between partners, reducing the relative taxable component of the total superannuation balance and others.

The clear takeout from the above is that although the after-tax effectiveness of a Transition to Retirement Strategy has been reduced by the changes applying from 1/7/2017, there are still potential financial benefits. These benefits are of course, in addition to other non-financial benefits that can flow from such strategies.

Things to consider

Keep in mind there are some technical issues around Transition to Retirement Strategies that should be fully considered in the light of the personal circumstances of the individual including:

- Member age: Not everyone can access a TTR pension – it is only accessible when you reach preservation age, which for most is the age of 60.

- Withdrawal cap: The amount that you withdraw each year is capped at 10% of the balance of the pension. This means you may need to top up this account through contributions in the years prior so that you have smooth cash flow.

- Total superannuation balance: Accessing a TTR pension can mean that you exhaust your retirement savings earlier. Your savings may need to last for up to 30 years and withdrawing these funds early may have a significant impact in later years. Plan carefully and calculate the funds available to you today and how this may impact your retirement savings.

- Income level: A TTR pension is not a ‘set and forget’ strategy. An annual review of your plan should be done so that income streams and contributions can be fine-tuned to fit your situation.

Lastly, not all super funds offer TTR pensions, so speak to an adviser and seek appropriate personal advice before making any decisions.

The information provided in this article is general in nature and does not consider your circumstances, needs, objectives or financial situation. This information does not constitute financial or taxation advice. Before acting on any information in this article, you should consider its appropriateness concerning your personal situation and seek advice from an appropriately qualified and licensed professional.

BOB LOCKE – CHARTERED ACCOUNTANT & SMSF SPECIALIST

Bob Locke has been an accountant and taxation expert for 35 years. His company, Practical Systems Super, provides an all-in-one SMSF solution with a full administrative service, SMSF management software, and independent, licensed advice, tailoring their package to meet the individual needs of trustees and SMSF professionals.

To find out more about Practical Systems Super, visit www.pssuper.com.au, or call 1800 951 855.

Early access to your super when the going gets tough

With the prolonged drought and bushfires affecting many farmers and rural businesses across the country, questions are often raised about accessing existing superannuation to ease their financial stress.

When going through difficult times, it may be frustrating that you aren’t able to access your superannuation account, especially when you need it the most. If you are experiencing severe financial hardship or have a medical disability you just can’t afford, you may have the right to apply to have some of your superannuation released before you retire.

Eligibility for early release of benefits

Superannuation is meant to be a long-term investment to provide benefits in retirement (or death benefits). To qualify for all the tax and associated benefits, a superannuation fund must have this as its “sole purpose”.

Once a person reaches the age of 65 (or dies), access to their superannuation is unrestricted. Prior to that time, one may be able to access the money before retirement if the person meets an alternative “condition of release,” often in dire situations such as a total and permanent disability or terminal illness.

However, the superannuation legislation also recognises that there can be other legitimate situations where the release of monies before the intended time may be appropriate, these include:

- Compassionate grounds – to cover items such as; medical expenses, home modifications to cater for disability, housing loan payments to prevent foreclosure and funeral expenses of dependents

- Severe financial hardship – for amounts up to $10,000 in any year

- Transition to retirement – provided the person has reached their “preservation age”

Applying due to severe financial hardship

If you’ve spoken to a financial adviser/counsellor and are confident that early access to superannuation is the right course of action, you can apply for early release based on severe financial hardship. The rules for accessing super on the grounds of financial hardship are quite specific, limited in their application and are often misunderstood.

You are eligible for access under financial hardship if you:

- Are unable to meet reasonable and immediate living expenses such as mortgage payments, rent arrears, medical expenses etc.

- Are receiving an income support payment

- Have been receiving income support payments for at least 26 weeks in a row

A super withdrawal due to severe financial hardship is paid and taxed as a super lump sum. If the condition is met, you will be limited to withdrawing a maximum of $10,000 within a 12-month period.

The eligibility rules are different if you’re over “preservation age” and haven’t retired. You must:

- have reached your preservation age plus 39 weeks

- not be gainfully employed

- have received the income support payments for at least 39 weeks since reaching preservation age

How to apply

Applications for release of superannuation on compassionate grounds must be made to the Australian Taxation Office. Applicants need to provide appropriate documentary evidence to prove the intended use of the funds and demonstrate that the expenses could not be met from alternative sources. Importantly, the relevant expenses must not have already been paid. If approved, the Taxation Office will issue an authority to the fund concerned for a release of the funds.

Applications based on severe financial hardship are made to the trustee of the fund concerned. The general requirement is that the applicant must have been on some form of government support payment for a minimum of 26 weeks and can demonstrate financial hardship. In the case of self- managed superannuation funds, the trust deed of the fund should be checked to ensure that it allows for such payments.

Example – financial hardship:

Fred and Lucy are farmers in their early fifties whose financial situation has been severely impacted by the continuing drought. Their cash reserves have been exhausted by continuing feed bills for their remaining livestock. They have been receiving Farm Household Allowance for the past nine months and are struggling to pay for basic living expenses including food and school expenses for the children. They have a self-managed superannuation fund with balances of $350,000 each.

Fred and Lucy could apply to the trustee on the basis of severe financial hardship for the release of up to $10,000 each. This would need to be properly documented and their position verified with appropriate evidence.

Note that as Fred and Lucy are under their “preservation age”, any financial hardship payments would be treated as taxable lump sums – the final amount of tax applicable will vary depending on the taxable/tax-free components of their balances and their other taxable income – it could range from 0% to 22%.

Transition to retirement

Transition to retirement strategies can provide a legitimate means of accessing superannuation benefits before normal retirement. The important qualifier here is that the person must have reached their preservation age which will range from 55 to 60 depending on the year of birth. The following table illustrates this:

| Date of Birth | Preservation age |

|---|---|

|

Before 1/7/1960 |

55 |

|

1/7/1960 to 30/6/1961 |

56 |

|

1/7/1961 to 30/6/1962 |

57 |

|

1/7/1962 to 30/6/1963 |

58 |

|

1/7/1963 to 30/6/1964 |

59 |

|

After 30/6/1964 |

60 |

Example – transition to retirement strategy

John and Noelene are cattle graziers who have planned well for recurring drought conditions. In good years they have invested in additional superannuation contributions to their self-managed fund and both have accumulated Farm Management Deposits. The current severe drought conditions have placed considerable strain on the family budget. They are keen to maintain their breeding stock and plan to progressively draw down the FMDs to fund fodder and supplements. This will ensure that when the drought breaks, they will be well placed to quickly rebuild and generate solid cashflows. In the meantime, they estimate they will require up to $100,000 per annum to assist with living expenses and pay the fees for their twin boys who are in their final two of years at boarding school.

John is 60 and has $1 million in superannuation and Noelene is 54 and has $700,000 in her superannuation account. After taking appropriate advice, John decides to commence a transition to retirement pension with the full balance of his accumulation account. He will be required to withdraw the minimum amount of 4% ($40,000) and can draw up to the maximum of 10% per annum – that will allow for the withdrawal of up to $100,000 per annum. Note that Noelene could not follow this strategy as she has not yet reached her preservation age and therefore has not satisfied a condition of release. As John has turned 60, the receipt of the pension amounts from the fund will be tax-free in his hands.

Once the drought breaks and normal cashflows return, they plan to commute the transition to retirement pension back to accumulation phase and top-up contributions as their financial position improves

Risks of accessing your super early

While accessing your superannuation may seem like an easy solution when going through a financial crisis, it is important to consider all the associated risks and consequences. Individual circumstances vary and these can include:

- Tax may apply to withdrawals

If you are below preservation age, you may be required to pay tax on any money you get from your superannuation. The tax varies depending on your circumstances and the taxable/tax free components of your superannuation balance.

- Fees & charges

You may need to pay your super fund a fee to have your super released early.

- Reduced retirement benefits

Early withdrawals can have compounding effects on the future balance of your superannuation with consequential impacts on your retirement plans.

- Impacts on other government benefits

Changes to your income due to superannuation benefits received may affect your eligibility for other benefits such as Family Tax Benefit, childcare allowance, etc.

- Watch out for scams

In recent years there have been a number of so-called “early access” schemes that have been promoted to facilitate the illegal early release of monies from superannuation accounts. Appropriately, the regulators have acted promptly against these schemes and there are severe penalties for promoters and trustees who engage in this unlawful conduct.

The information provided in this article is general in nature and does not consider your circumstances, needs, objectives or financial situation. This information does not constitute financial or taxation advice. Before acting on any information in this article, you should consider its appropriateness concerning your personal situation and seek advice from an appropriately qualified and licensed professional.

BOB LOCKE – CHARTERED ACCOUNTANT & SMSF SPECIALIST

Bob Locke has been an accountant and taxation expert for 35 years. His company, Practical Systems Super, provides an all-in-one SMSF solution with a full administrative service, SMSF management software, and independent, licensed advice, tailoring their package to meet the individual needs of trustees and SMSF professionals.

To find out more about Practical Systems Super, visit www.pssuper.com.au, or call 1800 951 855.

The information provided in this article is general in nature and does not take into account your personal circumstances, needs, objectives or financial situation. This information does not constitute financial or taxation advice. Before acting on any information in this article, you should consider its appropriateness in relation to your personal situation and seek advice from an appropriately qualified and licensed professional.

Make the most of your super with a personal deductible contribution

Would you like more flexibility with your superannuation but don’t have the option to salary sacrifice? You can now claim a tax deduction on your personal contributions. SMSF expert Bob Locke explains.

How much can you contribute?

Under the current rules, the maximum amount of “concessional” superannuation contributions that can be claimed as a tax deduction is $25,000.00 per person per annum. This is referred to as the “Concessional Contributions Cap”. This amount includes any super contributions paid by your employer; salary sacrifice contributions plus any other tax-deductible personal contributions you make to your super account.

On the other hand a “non-concessional” contribution is a payment made to superannuation after tax. It can be from a range of sources such as an inheritance, additional payment from your after-tax salary, property sale etc. The usual cap on non-concessional contributions is $100,000 per financial year.

Salary sacrifice vs PersonalContributions

Until 30 June 2017, only the self-employed, retirees or those who earned less than 10% of their income as an employee, could claim a tax deduction on a personal contribution.

This restriction meant that many employed individuals could not make deductible personal contributions to reduce their taxable incomes. The only way to maximize their total concessional contributions cap was to make arrangements with their employer for a salary sacrifice arrangement where they would reduce their gross salary in favour of the employer making a larger contribution (above the normal 9.5% of salary) to the employee’s super fund.

Now there’s an opportunity to give your super investment a boost and reduce your tax bill at the same time. With the changes effective from 1 July 2017, employees can make additional personal contributions and claim a tax deduction for the additional contributions, thus putting them on the same footing as self-employed people.

But how is that different from a salary sacrifice arrangement you may ask. Though salary sacrifice arrangements provide the same benefits one may not always be able to make such arrangements with their employer.

Compared to regular salary sacrifice contributions which can only be made prospectively a personal deductible contribution means you can make one lump sum contribution towards the end of the financial year. The additional flexibility of this system may be helpful in several different scenarios.

Take Mary’s case for instance. Mary works as a specialist teacher earning $110,000 annually. She has had an investment property for many years that she decides to sell in preparation for her impending planned retirement. On speaking to her accountant Mary finds out that based on the estimated sale price, there will be a taxable capital gain of $100,000 on the sale of the property which will cost her almost $45,000 in additional tax. She decides to make an additional contribution to superannuation of $14,500 and as a result, reduces her tax bill by around $7,000. Although Mary’s super fund will have to pay tax of $2,175 (15% of 14,500) on the additional contribution, she is still almost $5,000 better off.

Or take the case of Joe who is employed as a builder and earns $60,000 pa. In May, Joe receives a bequest of $25,000 from the estate of a recently deceased relative. He would like to retain around $6,000 of the money to take the family on a holiday trip and save the balance of $19,000. After talking to his financial adviser, Joe decides to contribute the full $25,000 to his existing superannuation fund; $19,000 is claimed as a concessional contribution and $6,000 as a non-concessional contribution.

As a result of claiming the additional contribution, Joe receives an additional tax refund of $6,800, which he uses for the family holiday. After allowing for the additional tax in the super fund on the concessional contribution of $2,850 (i.e. 15% of $19,000), Joe has increased his net savings by $3,150 and also has an additional $800 spending money for the holiday!

Super contributions over 65

Turning 65 years of age is a life milestone, but unfortunately, it does make putting money into your super a bit more difficult.

If you are over 65 you will need to pass the “work test” to continue making contributions – this means you will need to have worked a minimum of 40 hours in any 30-consecutive day period during the financial year.

Also, just like salary sacrifice superannuation contributions, Centrelink adds back any personal concessional contributions claimed when assessing entitlements that are subject to the “income test”.

Note that this age limit is proposed to increased to 67 from 01/07/2020.

Making extra contributions to your super

If you would like to make extra contributions to your superannuation, you can do it using either ‘before-tax’ or ‘after-tax’ money, keeping in mind that there are annual limits (caps) on how much you can contribute to superannuation.

Consider your financial situation and decide whether making extra super contributions is right for you across the short and long term.

Bob Locke – Chartered Accountant & SMSF Specialist

The information provided in this article is general in nature and does not take into account your personal circumstances, needs, objectives or financial situation. This information does not constitute financial or taxation advice. Before acting on any information in this article, you should consider its appropriateness in relation to your personal situation and seek advice from an appropriately qualified and licensed professional.

Christmas Trading Hours

Merry Christmas from the team at Practical Systems Super

We wish you and your family a joyous and safe Christmas.

Thank you for your wonderful support throughout the year, we look forward to working with you in 2020!

We will be closed from 5:30 pm, Monday 23rd December and reopen at 8:30 am on Thursday 2nd January.

If you have any questions regarding our services, please contact our office via email [email protected] or call the office on 1800 951 855.

Understanding SMSF Trustees

A Self-Managed Superannuation Fund (SMSF) is a type of “trust” and like any trust must be run by trustee/s. However, before setting up it is important to understand the SMSF trustee structure and rules.

Who is a Trustee?

An SMSF trustee is responsible for running the fund and making decisions that affect the retirement interests of each fund member. The Trustees are responsible for administering the SMSF duties including:

- Establishing the Investment Strategy

- Complying with all Super Laws

- Maintaining all records of the SMSF

- Lodging Tax and Regulatory Returns

Trustee Options

There are two SMSF trustee structure options available, one where the trustees work in their individual capacity and the second where a company is appointed as the trustee. Each option is detailed below.

In both cases, the members run the fund and as a general rule, all members are either trustees themselves or directors of the corporate trustee.

- Individuals as trustees: In this case, trustees who are individual people (as the name suggests) manage the fund and each trustee is a member. It is important to note that where an SMSF has individual Trustees, it is a legislative requirement to have a minimum of two Individual Trustees. In the case of a sole member fund, the member would need to appoint an additional person to act with them as joint trustees.

- A company as corporate trustee: In this option, if you have an existing established company you can nominate this Company to be the Trustee of the SMSF. If not, you can establish a company for a “special purpose”, where the sole purpose of the company is to act as Trustee for an SMSF.

Generally, all of the members will need to be directors of the trustee company. In the case of a sole member fund, that member can be the sole director of the trustee company

Trustee Rules & Exceptions

SMSF trustee rules state that:

- Trustees (or trustee directors) cannot generally be in an employee/employer relationship (unless they are related).

- Trustees cannot be paid by the fund for carrying out their trustee duties. However, they could be paid for professional services supplied such as bookkeeping, legal or taxation services.

- Trustees need to be Australian residents as the place of central management and control of an SMSF must always be in Australia.

- All trustees must sign a declaration acknowledging their roles and responsibilities.

- People acting as trustees must not be “disqualified persons” – for example, those who have been convicted of an offence involving dishonesty or who are undischarged bankrupts.

In an SMSF, all members of the fund must be trustees and all trustees must be members. However, some exceptions to this rule are:

- Where a member is under 18 years of age – they will require a representative to act as a trustee on their behalf

- Where a member loses capacity – they will also require a representative to act for them

- In the case of a single member fund – where the trustee is not a company, they will require an additional person to act with them as trustees

Individual or Corporate Trustee: making the right choice

Statistics from the ATO indicate that as of 30 June 2017, the majority (58.6%) of all SMSFs had a corporate trustee.

The current “best practice” recommendation from most professionals in the industry is to use a trustee company and it is evident that more than 80% of newly established funds have a corporate trustee. The reasons for this are varied but include:

- Sole member funds. Single-member funds with a corporate trustee can have a sole director and no additional trustees are required. As the sole Director and Shareholder of the Company, this gives one total control of the SMSF.

- Administration simplicity. Members can move in and out of a fund through death, marriage, divorce, etc. Where this occurs when the trustees are individuals, the fund will be required to change all of the ownership details of its assets and investments and this can be a daunting and time-consuming task.

On the other hand, changing the directors of a trustee company is very simple and no other changes are required to assets or investments

- Continuity when members change. Unlike other types of trusts which have a limited life (80 years) due to the “rule against perpetuities”, a superannuation fund is exempt from this and can last for multiple generations. A company lasts until it is wound up or deregistered.

- Concessional tax guarantee. The rules for SMSFs provide that where the fund has individual trustees, its sole or primary purpose must be to pay old-age pensions. Where funds have both member pension accounts and accumulation accounts this could be brought into question.

This may become more significant with the latest round of changes to superannuation law which limit the total amounts that can be held in pension accounts and may result in some cases where accumulation accounts are held long term. Having a company as a trustee will avoid these uncertainties.

- Asset protection. In the case of a fund being sued, individual trustees could potentially be liable but this would not normally be the case for directors of a trustee company.

- Borrowing. It is easier for an SMSF with a corporate trustee to borrow (via a limited recourse borrowing arrangement), as often lenders will insist that an SMSF has a corporate trustee.

- Reduced penalties. In the event that any super laws are breached, the ATO levies administrative penalties on each trustee per violation. If the fund has a corporate trustee and the trustee is charged a penalty, it is only charged one penalty amount and the directors of the corporate trustee are jointly liable to pay that penalty.

However, where a fund has individual trustees a penalty would be imposed on each individual trustee. For example, if the fund has four members the penalty is four times that of the penalty imposed on a corporate trustee for the same superannuation law infringement.

It is also generally recommended that the trustee of an SMSF should be a “special purpose superannuation trustee company”. This means that the company only acts in that single capacity and does not operate a business or act as trustee of another trust (these conditions are set out in the company’s constitution). The advantages of this approach include that there is no possible confusion over the separation/ownership of superannuation fund assets and the annual ASIC filing fees are only around 20% of the usual fee.

The additional one-off set up costs for a company trustee will generally be less than $1,000 (with annual filing fees of less than $50) but this represents good value in light of the advantages outlined above.

The information provided in this article is general in nature and does not take into account your personal circumstances, needs, objectives or financial situation. This information does not constitute financial or taxation advice. Before acting on any information in this article, you should consider its appropriateness in relation to your personal situation and seek advice from an appropriately qualified and licensed professional.